The Service-to-Cloud Multiplier

A Special Report by Rick Fulton

How Recurring Revenue Creates Disproportionate Enterprise Value

Why Google's $7.05 Rule, Microsoft's Cloud Strategy, and the SaaS Apocalypse Matter to Owners, Investors, and Acquirers

In this report, I examine the relationship between recurring revenue, customer retention, cloud adoption, and enterprise value including:

Google's $7.05 Multiplier

The Service-to-Cloud Multiplier

Revenue Quality vs Revenue Growth

Why Retention Drives Valuation

The SaaS Apocalypse and What It Changed

What Private Equity Firms Look For

Why Some MSPs Outperform Others

Executive Summary

Not all recurring revenue is created equal.

And in 2026, buyers know the difference.

A company generated revenue, produced EBITDA, and buyers applied a multiple.

Simple.

Then cloud computing, software subscriptions, and managed services changed the equation.

Suddenly, not all revenue was created equal.

A dollar of recurring revenue became worth more than a dollar of project revenue.

A dollar of cloud revenue became worth more than a dollar of traditional services revenue.

And a dollar of highly retained recurring revenue became worth dramatically more than either.

Two powerful concepts help explain why.

The first is Google's famous "$7.05 Multiplier," which demonstrates how recurring customers generate economic value far beyond their initial revenue contribution.

The second is what many investors refer to as the "Service-to-Cloud Multiplier," the phenomenon whereby businesses increase enterprise value by shifting revenue from one-time services to recurring cloud and managed services offerings.

Together, these concepts help explain one of the most important trends in modern technology M&A:

Enterprise value increasingly follows recurring revenue quality rather than revenue quantity.

However, the market correction that followed the SaaS boom fundamentally changed the conversation.

The "SaaS Apocalypse" exposed a critical truth:

Not all recurring revenue deserves a premium valuation.

Today, sophisticated buyers evaluate recurring revenue through a more demanding lens.

The result is a new valuation framework that rewards durable, profitable, and highly retained revenue streams while penalizing recurring revenue that lacks economic substance.

Part I: Google's $7.05 Multiplier

Why One Customer Can Be Worth Far More Than One Dollar

The Google $7.05 Multiplier originated from a simple observation:

A customer is not worth the revenue they generate today.

A customer is worth the future cash flows they are likely to generate over time.

This idea transformed how technology companies viewed customer acquisition.

Rather than focusing exclusively on current revenue, leading companies began measuring customer lifetime value.

The framework asks a simple question:

"If a customer generates one dollar of recurring revenue this year, what is the total economic value of that customer relationship?"

The answer often turns out to be several times greater than the original dollar.

The Economics Behind the Multiplier

Customer value is driven by four variables:

Revenue generated

Gross margin

Retention rate

Customer lifespan

A customer who generates recurring revenue for ten years is dramatically more valuable than a customer who leaves after one year.

Likewise, a customer producing high-margin recurring revenue creates more value than one requiring constant service delivery and support.

The lesson is straightforward:

Recurring revenue compounds.

Every renewal increases the economic value of the customer relationship.

Every year retained reduces acquisition risk.

Every additional service sold increases lifetime value.

This is the foundation upon which modern SaaS businesses were built.

Why Investors Became Obsessed With Retention

Retention is arguably the most important variable in the entire framework.

Consider two companies:

Company A retains 80% of customers annually.

Company B retains 95% of customers annually.

The difference appears modest.

In reality, the second company may possess customer relationships that last several times longer.

As retention improves:

• Customer lifetime value rises

• Revenue predictability improves

• Cash flow visibility increases

• Enterprise value expands

This principle eventually became one of the cornerstones of software investing.

Part II: Microsoft's Service-to-Cloud Multiplier

Why Revenue Mix Matters More Than Revenue Size

While Google focused on customer economics, Microsoft demonstrated something equally powerful at the enterprise level.

As businesses shifted from traditional IT services toward cloud subscriptions, recurring services, and managed offerings, valuation multiples expanded.

The reason was not revenue growth alone.

It was revenue quality.

A company generating $10 million of project-based revenue and a company generating $10 million of recurring cloud revenue may appear identical on an income statement.

To investors, they are fundamentally different businesses.

One must rebuild revenue every year.

The other begins each year with much of its revenue already committed.

This difference changes everything.

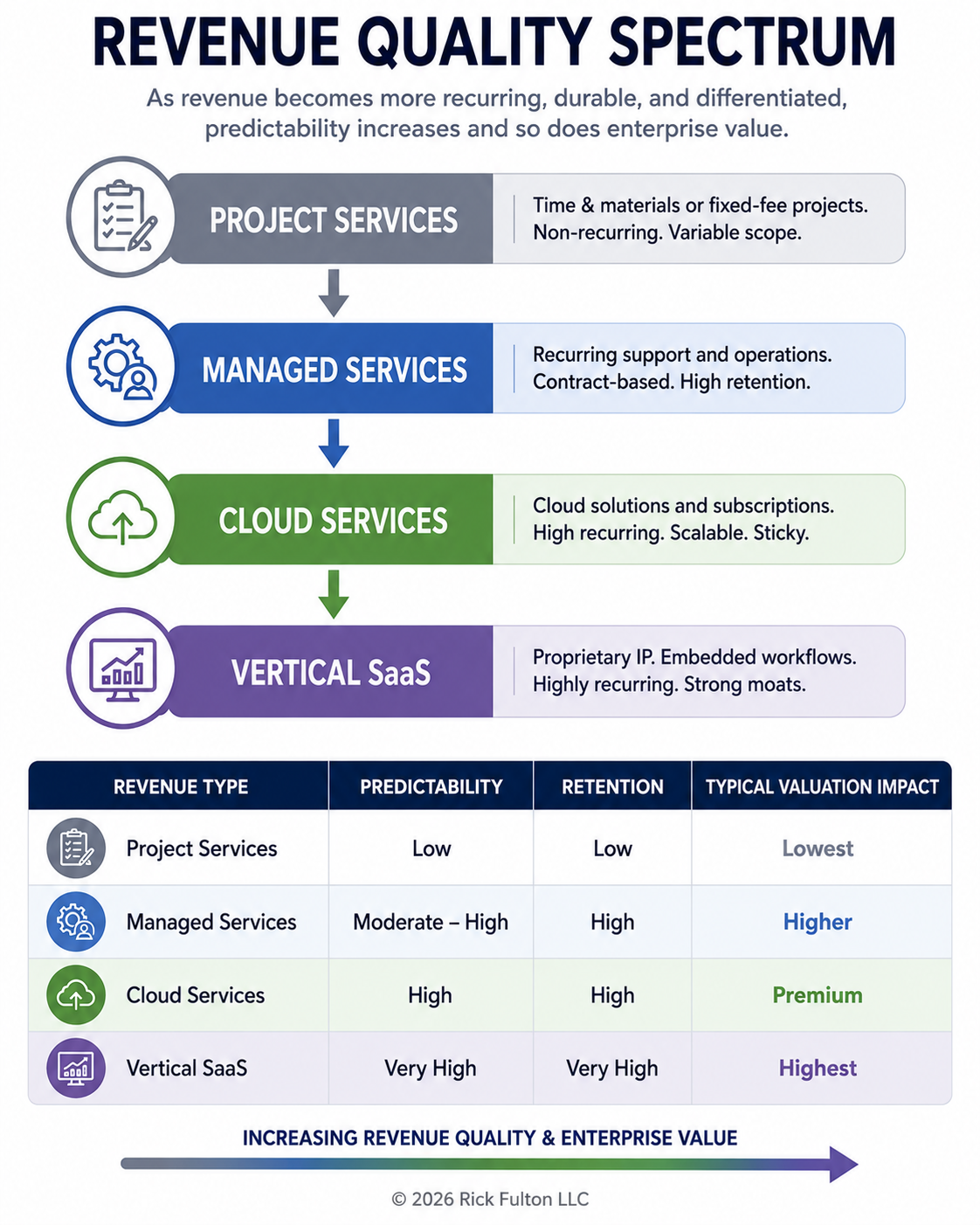

The Evolution of Revenue Quality

Technology businesses generally evolve through several stages.

Stage 1: Project Services

Characteristics:

• One-time engagements

• Revenue resets annually

• Low predictability

• Limited scalability

Typical valuation:

Lower multiples

Stage 2: Managed Services

Characteristics:

• Monthly recurring revenue

• Long-term customer relationships

• Contracted revenue streams

• Greater predictability

Typical valuation:

Higher multiples

Stage 3: Cloud-Centric Revenue

Characteristics:

• Subscription economics

• Automated delivery

• High retention

• Expansion opportunities

Typical valuation:

Premium multiples

The market consistently rewards businesses that move up this progression.

Not because cloud is fashionable.

Because future cash flows become increasingly predictable.

The Enterprise Value Effect

Imagine two companies.

Company A

Revenue: $20 million

Recurring Revenue: 20%

Project Revenue: 80%

Company B

Revenue: $20 million

Recurring Revenue: 80%

Project Revenue: 20%

Revenue is identical.

Enterprise value often is not.

Sophisticated buyers frequently assign materially higher valuation multiples to the second company because future revenue carries less uncertainty.

The Service-to-Cloud Multiplier is essentially the process of converting lower-quality revenue into higher-quality revenue.

When done successfully, enterprise value can increase far faster than revenue itself.

Part III: The SaaS Apocalypse

When Recurring Revenue Stopped Being Enough

For years, investors rewarded recurring revenue almost automatically.

Software companies with rapid growth commanded extraordinary valuation multiples.

Revenue growth often mattered more than profitability.

The assumption was simple:

Future growth would eventually justify today's valuation.

Then the market changed.

Interest rates rose.

Capital became more expensive.

Investors became less willing to pay enormous premiums for profits expected many years in the future.

Technology valuations compressed.

Many software companies lost substantial portions of their market value.

This period became known by many investors as the SaaS Apocalypse.

What the Market Learned

The correction did not prove that recurring revenue was unimportant.

It proved that recurring revenue alone was insufficient.

Investors became far more selective.

Questions changed.

Instead of asking:

"How fast is the company growing?"

Buyers increasingly asked:

• How profitable is growth?

• How durable is retention?

• How strong are margins?

• How dependent is growth on constant spending?

• How real is free cash flow?

The conversation shifted from quantity to quality.

The New Hierarchy of Revenue

The market increasingly views recurring revenue through three categories.

1. Weak Recurring Revenue

• High churn

• Low margins

• Heavy discounting

• Commodity offerings

Receives limited valuation premium.

2. Good Recurring Revenue

• Stable retention

• Predictable renewals

• Reasonable profitability

Receives meaningful valuation premium.

3. Exceptional Recurring Revenue

• High retention

• Strong cash flow

• Pricing power

• Mission-critical solutions

• Expansion opportunities

Receives substantial valuation premium.

The multiplier still exists. The requirements became stricter.

What This Means for MSPs and Cloud Providers

The SaaS correction created an interesting dynamic for managed services firms.

Unlike many venture-backed software companies, most MSPs generate real cash flow today.

They often possess:

• Long customer relationships

• Essential services

• High renewal rates

• Positive EBITDA

• Strong operating leverage

As a result, many high-quality MSPs remained attractive acquisition targets even while public SaaS valuations declined.

Why?

Because recurring revenue supported by actual profitability is exactly what modern acquirers seek.

The New Valuation Formula

The original lesson from Google's framework was:

One dollar of recurring revenue can be worth several dollars of enterprise value.

The lesson from Microsoft's Service-to-Cloud Multiplier was:

Shifting revenue toward recurring cloud services can dramatically increase enterprise value.

The lesson from the SaaS Apocalypse is:

Only durable, profitable recurring revenue deserves the full benefit of those multipliers.

The future of technology valuation is not about maximizing revenue.

It is about maximizing revenue quality.

Companies that successfully combine:

• Recurring revenue

• High retention

• Strong margins

• Positive cash flow

• Expansion opportunities

will continue to command premium valuations.

The Google $7.05 Multiplier explains why recurring customers matter.

The Service-to-Cloud Multiplier explains why recurring revenue matters.

The SaaS Apocalypse explains why quality matters.

If you are exploring acquisitions, partnerships, growth opportunities, or strategic alternatives within the Google or Microsoft partner ecosystems, I welcome the opportunity to connect.