Special Report:

Service-to-Cloud Multipliers and M&A Valuation by Rick Fulton

1. Market Shift: The Obsolescence of the Pass-Through Model

In the early 2020s, a partner could build a healthy business—and a decent valuation—simply by being a high-volume reseller of licenses. This is exactly what I did for many years!

In 2026, that era is over.

Both Google and Microsoft have structurally re-engineered their partner programs (Google Diamond Tier and Microsoft AI Cloud Partner Program) to prioritize "Consumption + Depth." Resale-only revenue is now viewed by institutional buyers as "low-fidelity" income.

Because the hyperscalers are squeezing margins on basic resale to fund AI infrastructure, a firm that doesn’t attach services is essentially a "depreciating asset."

The M&A Impact: "Resale-Heavy" shops are being acquired at 4x–6x EBITDA, while "Services-First" shops are commanding 12x–18x.

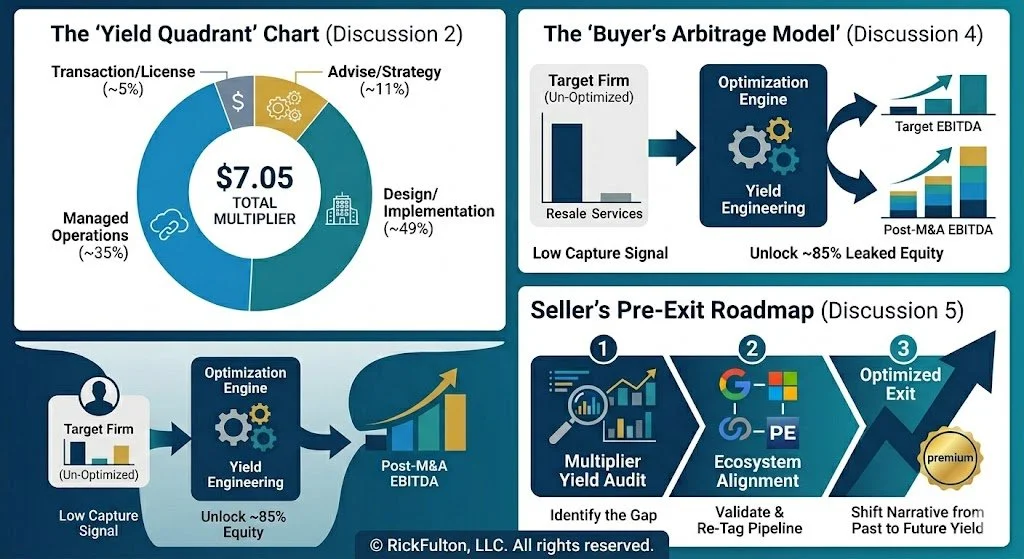

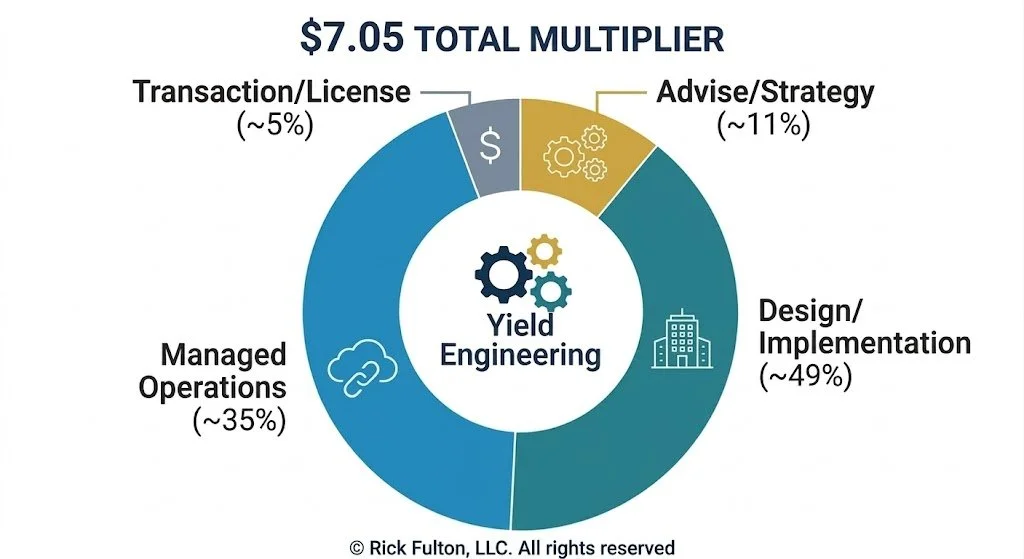

2. Economic Benchmarks: Decoding the $7.05 Ecosystem Multiplier

While the headline numbers are impressive, the value is in the Composition. I break down the revenue pull-through into four distinct "Yield Quadrants":

Strategy & Advisory (~11%): The "Why." High-margin consulting that sets the stage.

Design & Implementation (~49%): The "How." This is the heavy lifting of 2026—building the Agentic workflows.

Managed Operations (~35%): The "Always." This is the recurring revenue that PE firms use to underwrite the deal.

Transaction/License (~5%): The "Gate." This is no longer the destination; it is simply the entry point to the rest of the stack.

The fact that Google ($7.05) and Microsoft ($6.26) have converged in this range proves that the "Service-to-Cloud Ratio" is now a structural law of the tech economy.

3. Alpha Drivers: Quantifying the ‘Agentic AI’ Service Premium

Not all service hours are created equal. In 2026, we have moved past "Chatbots" into Agentic AI—autonomous systems that actually execute tasks.

The Margin Delta: Standard cloud migration services are currently commoditized. However, Agentic AI integration requires specialized data architecture (BigQuery/Vertex AI or Azure Fabric).

The Result: Firms with "Agentic AI" designations are currently commanding 22% higher billable rates and higher utilization scores. On your balance sheet, this shifts your "Service Revenue" from a labor-cost game to a high-value IP game.

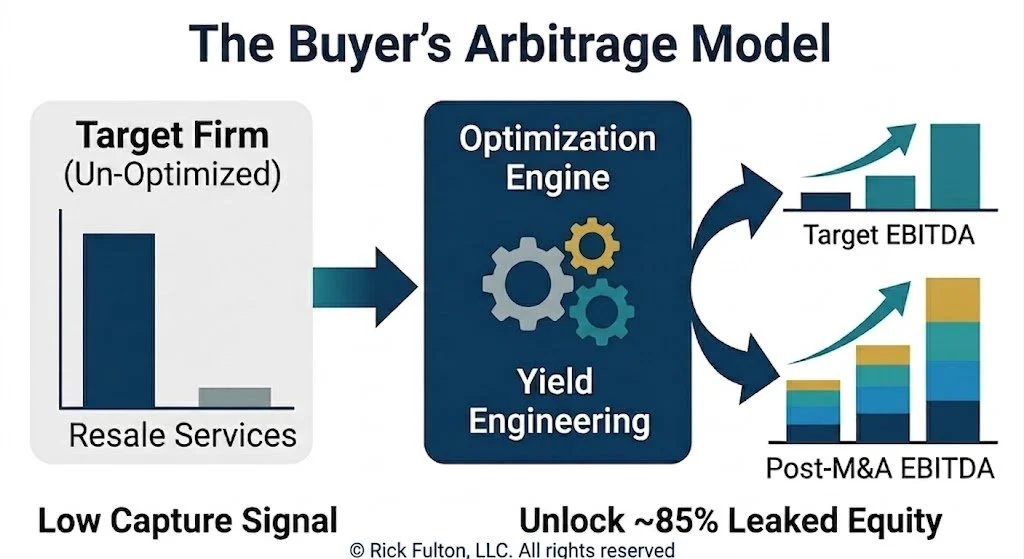

4. Due Diligence: Identifying Arbitrage via the ‘Capture Ratio

For Private Equity and Strategic Consolidators, the "Multiplier Gap" is the ultimate Arbitrage Signal.

The Diagnostic: If we find a target with $20M in Google Cloud consumption but only $3M in services, that is a "Low Capture" firm.

The Opportunity: A buyer can acquire that firm at a "Resale Multiple" (low), immediately plug in a high-performance services team, and "capture" the missing $60M+ in addressable service revenue.

Our Role: We conduct "Multiplier Due Diligence" to tell buyers exactly how much "unlocked" equity is sitting in the target's existing customer base.

5. Equity Optimization: The Roadmap to a Maximum-Yield Exit

For Founders, understanding the math is the difference between a "Retirement Exit" and a "Legacy Exit." We use a "Pre-Exit Yield Audit" to shift the narrative before you go to market:

Isolate the Tiers: We strip your P&L to show exactly where you are hitting the $7.05 mark and where you are leaking.

Validate the Pipeline: We help you re-tag your pipeline as "Ecosystem-Validated" revenue, which carries higher weight in a 2026 valuation.

The Multi-Cloud Story: If you are a Google shop, we show you how to add a "Microsoft Governance" layer to capture the $6.26 multiplier on the same client base, doubling your potential valuation surface area.